Airbnb: What the Bears Are Missing (Part 1)

An accelerating flywheel, a widening moat—and a market still extrapolating the past.

Note: This is Aquitaine’s second post on Airbnb, following a shorter thesis preview published in November. The full write-up is long overdue, owing, unfortunately, to a difficult stretch of family circumstances. While Airbnb’s stock has since risen significantly, I continue to believe the setup remains attractive for long-term investors.

This piece was finalized before Airbnb’s May 7 earnings call; any relevant updates will be incorporated into Part II. I hope the wait proves worthwhile.

Introduction

“Certain people believe things for understandable reasons. But those reasons are nonetheless bad reasons.” — Sam Harris

Warren Buffett has often remarked that it takes years to build a reputation and only minutes to destroy one. The reverse, however, may be just as true.

Consider Marie Antoinette: for more than two centuries, she has been remembered, above all, for a line she almost certainly never uttered, “Let them eat cake.” The myth survived not because the evidence was strong, but because it was memorable, convenient, and easy to repeat. The truth, by contrast, required context—and context has never traveled quite as efficiently as a good accusation.

This phenomenon perfectly describes the lingering reputation of Airbnb co-founder and CEO Brian Chesky. For those unfamiliar, Chesky acquired the label of “overhyper” several years ago. While the charge was not entirely without basis, it has been repeated far more often than it has been critically examined.

A closer look at the record reveals a much more nuanced reality. Chesky’s track record does not show a pattern of grand promises collapsing upon contact with reality; rather, it shows an unusually animated CEO whose rhetoric occasionally ran ahead of his intended message. (That same zeal has undeniably contributed to immense wealth creation, but that is a separate matter.)

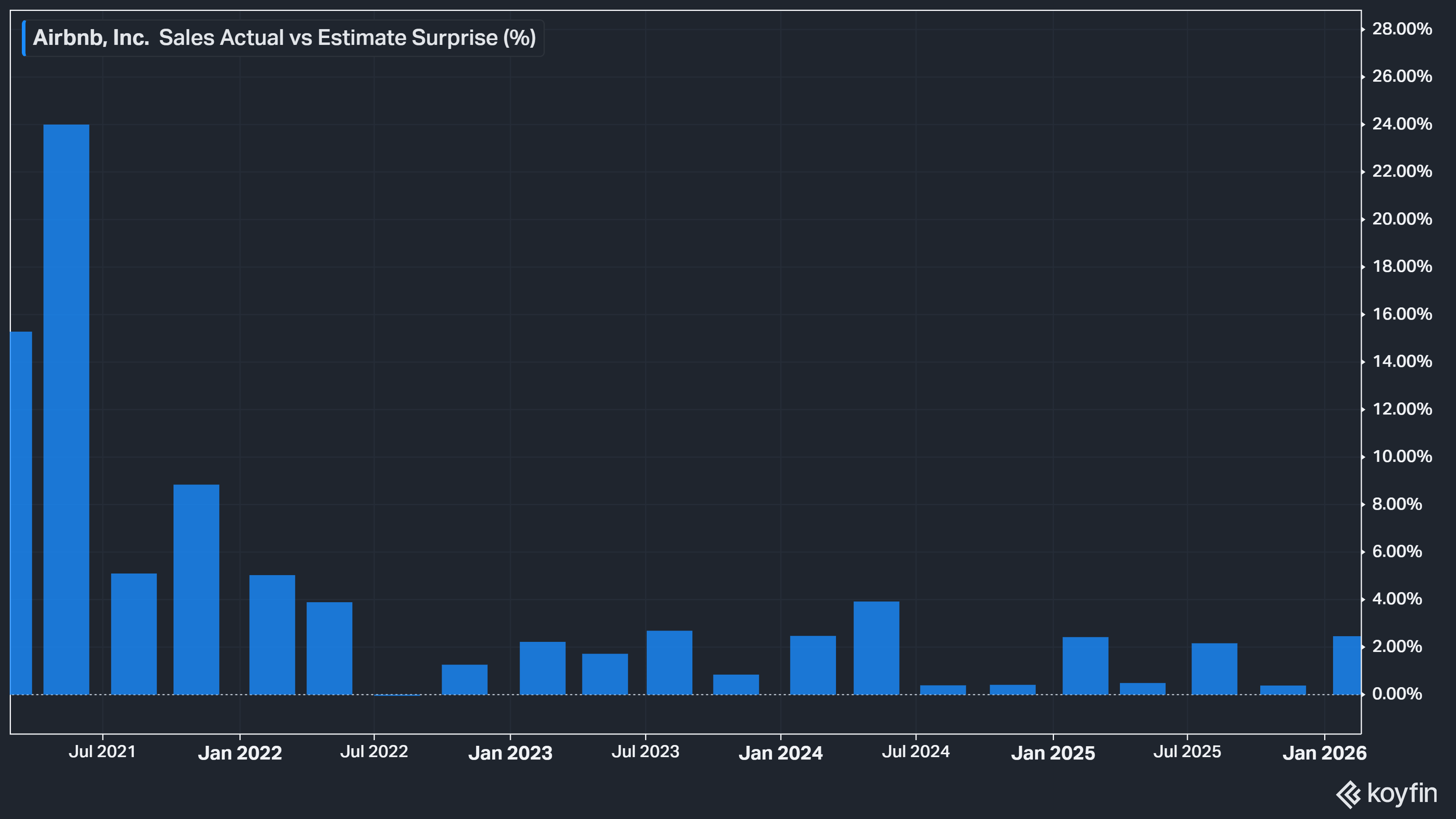

Since going public in 2020, Airbnb has met or exceeded consensus expectations for revenue and EBIT in all but one quarter. The supposed overhype, then, was rhetorical rather than financial—a crucial distinction.

Today, Chesky’s commentary is discernibly more restrained, suggesting he has learned from past scrutiny. He has also spoken openly about his suspected neurodivergence, which offers a more charitable—and likely more accurate—lens through which to understand what might otherwise be perceived as a genuinely disconcerting trait in a CEO.

While his reputation for overhyping no longer dominates investor discourse, it is still mentioned often enough to matter. It therefore remains, at minimum, a subtle interpretive filter through which Wall Street receives new information, causing current evidence to be discounted before it is properly weighed.

This lingering skepticism goes a long way toward explaining the striking divergence between Airbnb’s own medium-term financial outlook and the far more tempered expectations embedded in Wall Street estimates.

This mismatch is especially notable given that Chesky’s recent “implied guidance” has, in fact, been highly predictive. In September, for example, he expressed dissatisfaction with Airbnb’s roughly 10% growth rate—arguing that the company should be growing at least in the teens—before adding:

“I believe we are going to accelerate growth next year. I firmly believe that. I don’t want to overpromise what we’re going to do. But I don’t think people should take our deceleration and extrapolate that forward.”

Extrapolate they did.

In the weeks leading up to Q4 earnings, Chesky again signaled a reacceleration—both within the quarter and beyond. Even so, the stock fell more than 10% in the weeks that followed. Then came the print: just as Chesky had telegraphed months earlier, Airbnb reaccelerated in Q4 and guided to at least low-double-digit revenue growth for 2026.

Reputation, however, is only part of the story. Also relevant is what we might call a distribution problem—one I suspect will be resolved during the next earnings call or Summer Release.

Investors are conditioned to expect material information to surface through formal channels: filings, earnings calls, and press releases. Most of the time, that is exactly where it appears. Occasionally, however, important signals emerge in less obvious places, such as interviews, podcasts, or offhand remarks, where they are easier to miss and, consequently, easier to misprice. That appears to be the case here.

Before getting to the specifics, some context is needed. For those less familiar, 2025 was a pivotal year for Airbnb, arguably its most consequential from a product standpoint since the company’s founding. It launched three new businesses: Services, “reimagined” Experiences, and Hotels, specifically boutiques and independents. (While Airbnb has long had a small number of hotel listings on the platform, for reasons discussed later, they amounted to little more than a rounding error relative to what is now being built.)

Each of these new ventures, according to management, has the potential to generate billions in incremental revenue. Yet while their commentary has been highly bullish, it has also been carefully noncommittal.

Initially, Chesky suggested that these businesses could take three to five years to scale, which he effectively defined as reaching roughly $1 billion in revenue. He was also careful to add that not all of them would necessarily get there. By the Q2 2025 earnings call, however, his language had moved a notch higher, stating:

“I think each of these could easily be a multibillion-dollar business.”

The shift was subtle, but not trivial: the $1 billion benchmark had become multibillion, and the word “easily” nudged the implied floor higher still. The “could,” however, continued to leave room for ambiguity. CFO Ellie Mertz, meanwhile, remained more restrained in both scope and timing, using phrases like “significant contribution,” “material scale,” and “multiyear path.”

Beyond that, nothing in subsequent earnings calls—or in the many interviews and podcast appearances Chesky gave following the 2025 Summer Launch—strayed from this calibrated framing. (For readers who want the full chronology, I’ve compiled the verbatim remarks from both Chesky and Mertz [here], with timestamped links where possible.)

There was, however, one notable exception: an interview Chesky gave in January. The first real break came in his discussion of hotels. Noting that people often fail to realize the sheer size of the hotel industry, which is larger than the advertising industry dominated by Google and Meta, he stated:

“We do not need a large market share of hotels to have a huge business. Hotels will absolutely be a multibillion-dollar business.”

He offered a striking example, revealing that there were over 400 million searches for New York City on Airbnb last year. Given that Airbnb is “essentially banned” in New York, he pointed out that adding hotels means the company “can make quite a bit of revenue” there.

Two things stand out from this exchange.

First, the language was unequivocal. Gone were the earlier qualifiers and hedges; in their place was the definitive “will.”

Second, the anecdotal framing became hard data. Chesky had previously alluded to “millions and millions” of searches for New York City each year on Airbnb—a phrase that, though delivered with notable emphasis, dramatically understated the 400-million-plus reality.

Listeners do not infer magnitude from tone alone; they infer it from ordinary language conventions. Most would therefore have assumed a figure in the single-digit millions, reasoning that if the actual number were in the tens—or especially hundreds—of millions, he would have explicitly said so.

He also raised the implied floor on promoted listings, which are likely to roll out later this year or next, noting, “I think advertising is another multibillion-dollar business—it’s at least a billion dollars.” But the clearest break came when discussing the trajectory of these new businesses collectively:

“We basically put a horizon of three to five years for these to be multibillion-dollar businesses.”

Publicly, Airbnb had not quite done that—at least not explicitly. That suggests Chesky was either conflating internal assumptions with external commentary, or believed he had already been more precise than he actually was. Either way, the implications are significant.

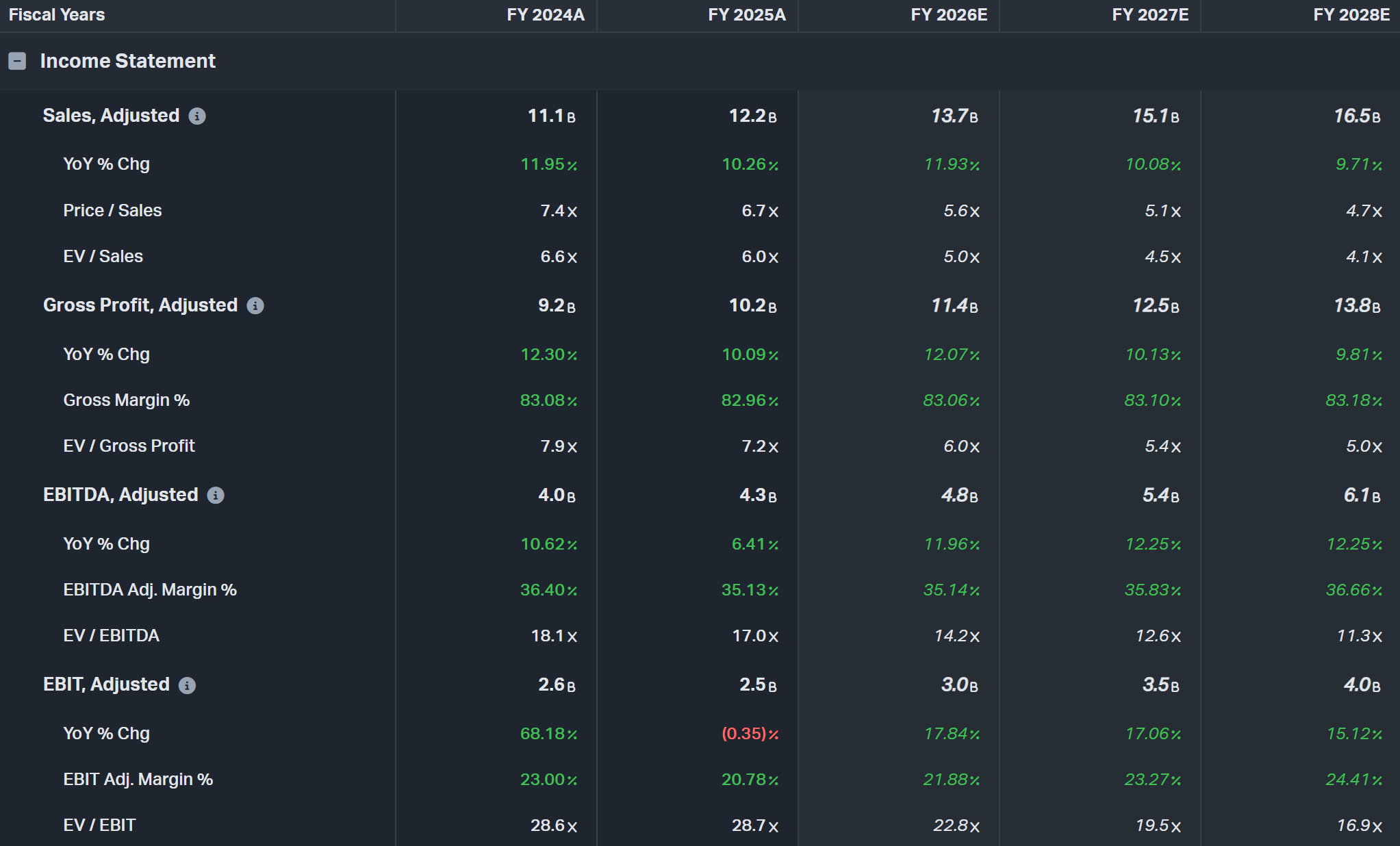

Taken at face value, the comment implies that consensus revenue estimates for 2028 through 2030 may be understated by at least $3 billion to $8 billion, before assigning any additional value to growth in Airbnb’s core business. (For reasons discussed later, I believe further core growth is also highly likely.)

That estimate also excludes any contribution from additional billion-dollar businesses not yet disclosed, despite management’s expectation that Airbnb can launch at least one new billion-dollar business per year for the foreseeable future.

Now, to address the elephant in the room: while I clearly find Chesky far more credible than most, the investment case does not depend on taking his projections at face value.

Fortunately, we know enough about the underlying assumptions—and have ample supporting data—to stress-test the case ourselves. That includes the major sources of debate and concern, such as AI disintermediation, heightened competition, and regulatory challenges, all of which will be covered in depth in Part II.

Having done that work, my conclusion is that Airbnb is likely to substantially exceed topline estimates while also outperforming on operating margins. Before we can chart the path ahead, however, we first need to establish its starting coordinates.

Disclosure: I and/or accounts under my control are long ABNB. This is not investment advice, but my opinion as of today, which may change quickly and without prior notice. Readers should conduct their own due diligence. Some quotes may be lightly edited for clarity and relevance.

Brief History

Airbnb’s origin story has been told often enough that there is little value in revisiting it at length here. For readers interested in the fuller version, Acquired’s 2020 episode remains the best single treatment. What follows instead is a high-level sketch of how the business evolved.

Airbnb—then known as “Airbedandbreakfast.com”—began as a low-cost substitute for hotels, used mostly by younger, budget-conscious travelers. Early listings were often spare rooms in occupied homes, and demand skewed heavily toward cross-border travel. Over time, however, both the platform and its user base moved steadily upmarket—a shift helped, in no small part, by the fact that many early Airbnb users aged into higher income brackets.

As inventory moved increasingly toward entire homes and apartments, Airbnb’s value proposition also changed. The appeal was no longer simply lower prices. It was more space, more flexibility, and a different kind of travel experience: the promise, as the company once framed it, of “living like a local.” Today, private rooms account for less than 10% of listings.

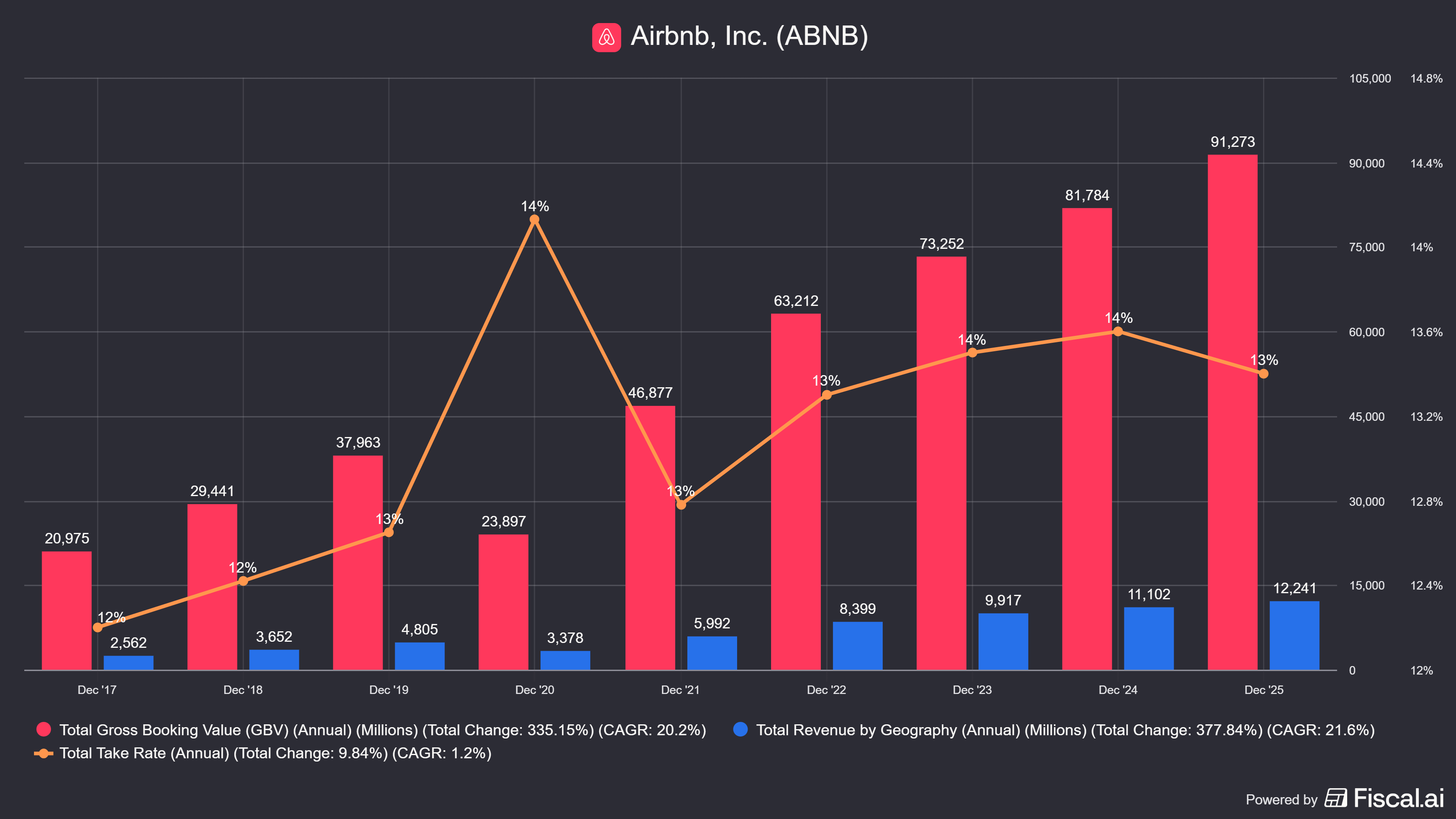

By 2019, Airbnb had reached nearly $40 billion in gross booking value and almost $5 billion in revenue. It had also become one of the most recognizable consumer internet companies in the world. What it had not yet become was profitable.

Then came the pandemic. Within weeks, Airbnb lost roughly 80% of its business and cut about a quarter of its workforce. At the time, the shock looked potentially existential. Yet the business recovered with surprising speed. Cross-border travel gave way to domestic trips, and average stays lengthened as remote work untethered millions of people from the office.

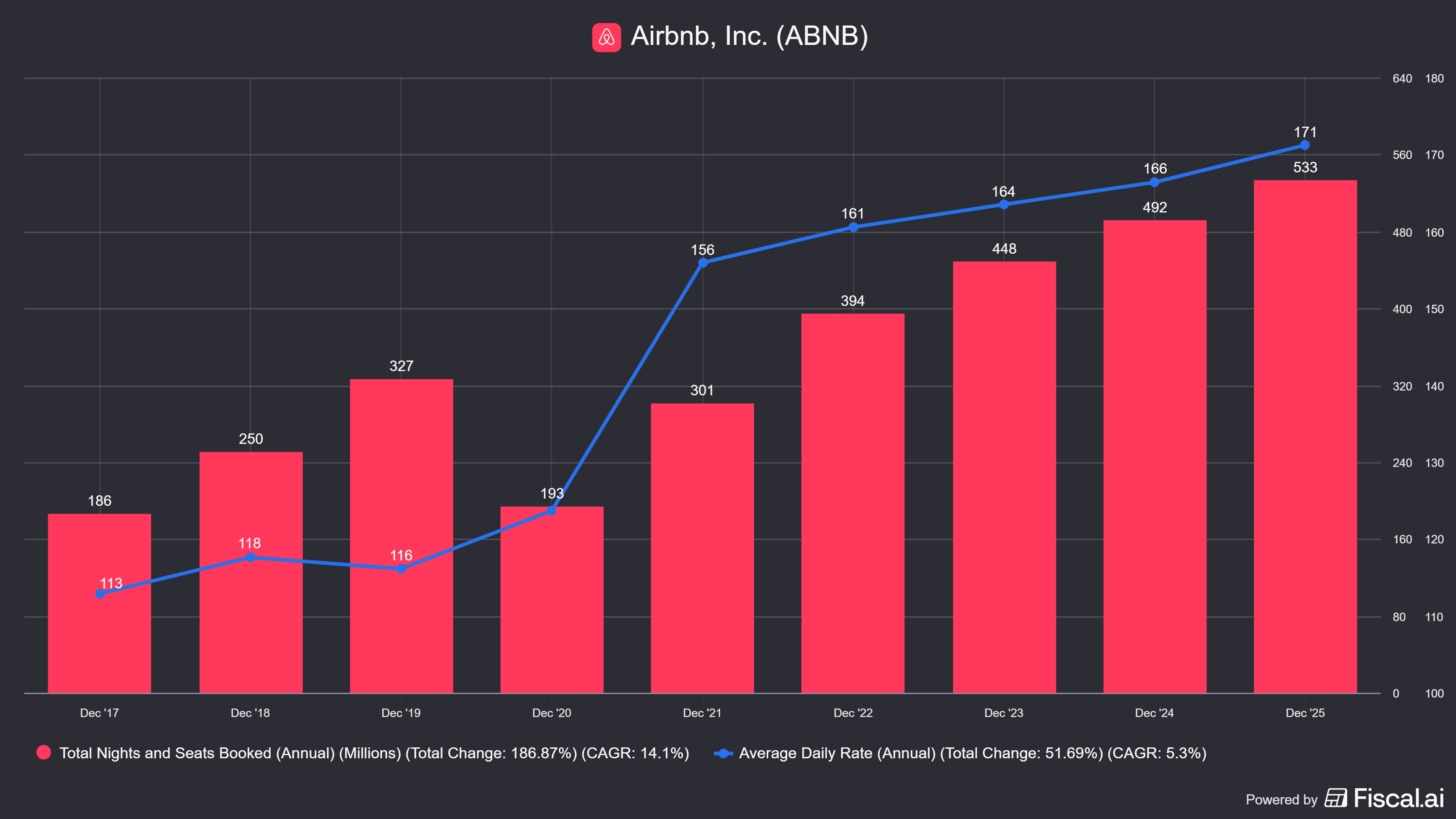

The pandemic also spurred a sharp increase in family and group travel, contributing to higher average daily rates (ADRs). Some of these effects have since moderated, but several remain structurally above pre-pandemic levels. Stays of 30 days or longer, for example, have settled at roughly 17% to 18% of nights booked, up from about 14% in 2019, though below the 20%-plus peak reached during the pandemic. The average trip length is now roughly four days.

Airbnb went public in late 2020 at $68 per share. The stock reached more than $140 on its first day of trading, making it one of the year’s standout IPOs. At the time, the three co-founders—Chesky, Joe Gebbia, and Nathan Blecharczyk—collectively owned about 42% of the company, with near-equal stakes and near-total voting control.

As of April 2026, they still held roughly 27% of the economic interest—with Chesky and Blecharczyk together owning about 22%—while continuing to control approximately 81% of the vote. Joe Gebbia is no longer involved in day-to-day operations but remains on the board.

Airbnb turned profitable in 2021 and now generates some of the highest free cash flow margins in the S&P 500, though not without caveats—including a notably heavy stock-based compensation (SBC) load.

Business Model and Overview

“Our core business could easily be two to three times bigger—and we did $80 billion in bookings last year.” — Brian Chesky, June 2025

The beauty of Airbnb’s marketplace model is that, unlike hotels, it “doesn’t have to pour concrete,” as Chesky put it. Airbnb doesn’t own or operate the properties on its platform; it connects guests with hosts, facilitates the transaction, and takes a fee. The result is music to every investor’s ears: asset-light, scalable, and capable of producing robust margins.

That advantage is reflected in its market cap, which, until very recently, was exceeded that of any single hotel operator in the world.

And yet the hotel industry itself remains far larger than the short-term rental (STR) market. In the U.S., Airbnb’s largest market, the company still accounts for only about one in ten nights away from home. The other nine go to hotels. We’ll return later to why travelers choose one over the other.

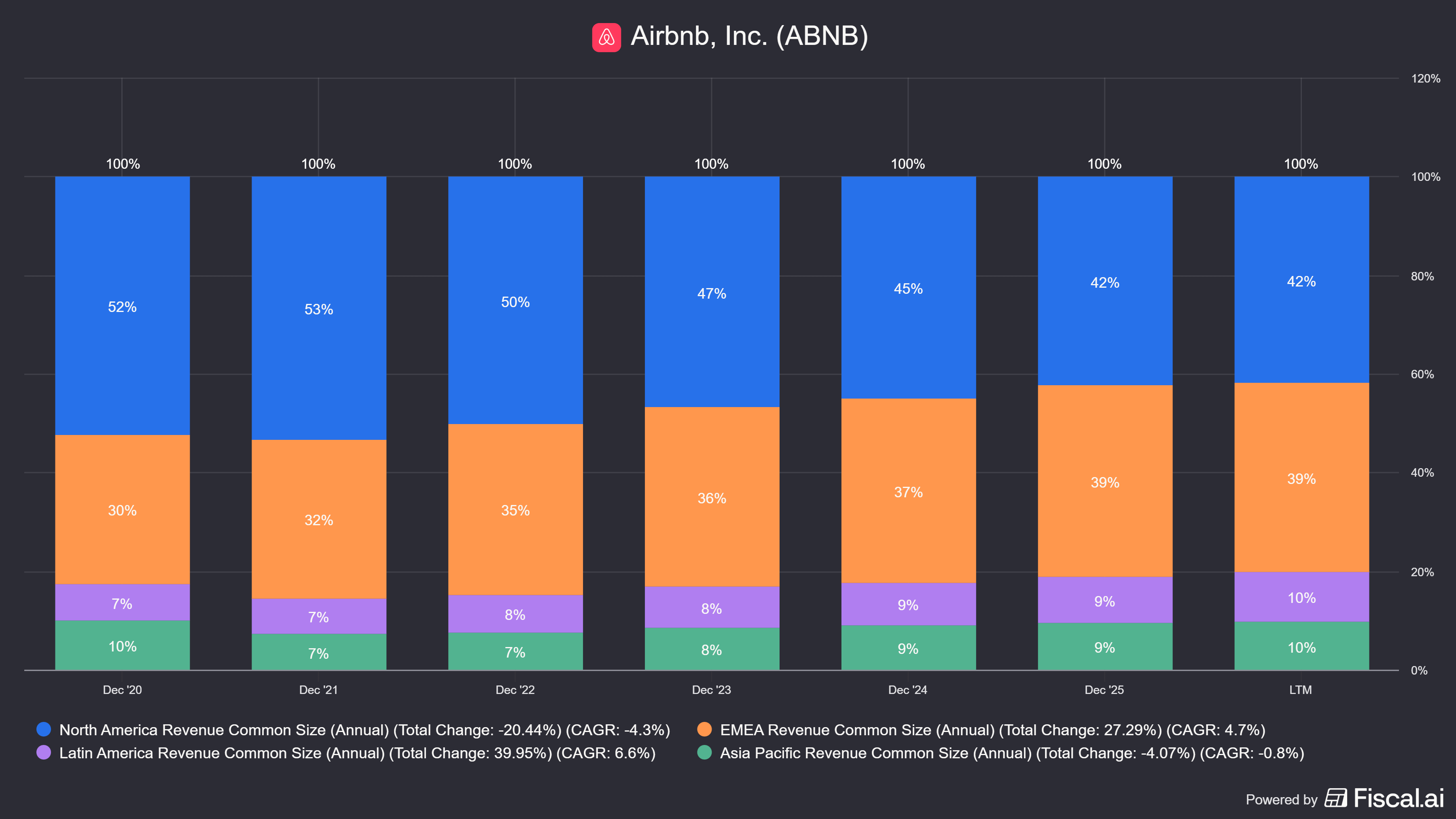

Today, Airbnb has more than 9 million active listings across 220-plus countries. Despite that global footprint, the business remains concentrated in a handful of mature markets. Roughly 70% of revenue comes from just five countries: the U.S., U.K., France, Canada, and Australia.

By volume, EMEA accounts for the largest share of nights and experiences booked, at roughly 40%, followed by North America at about 30%, Latin America at 17%, and Asia-Pacific at 13%. From a revenue standpoint, however, North America remains disproportionately important, as shown below.

Airbnb now has more than 5 million hosts, around 90% of whom are individuals—which makes it the largest non-professionalized supply base in the world by a wide margin.

For most hosts, Airbnb remains a source of supplemental income rather than a full-time business. Around 55% are women, and common host occupations include schoolteachers, healthcare workers, and students. In the U.S., the average host now earns roughly $15,000 per year, up from less than $10,000 five years ago.

Historically, Airbnb’s supply growth has been largely organic. More than 30% of hosts were previously guests, while word-of-mouth continues to play an important role in bringing new supply onto the platform. This is made easier by the fact that roughly half of new hosts receive a booking within three days, and 75% do so within nine—significantly faster than on competing platforms.

Large events have also proved to be powerful supply catalysts. During the Paris Olympics, more than 700,000 guests stayed in Airbnb listings, while roughly 50,000 new listings were added to the platform. About 80% of those remained active afterward.

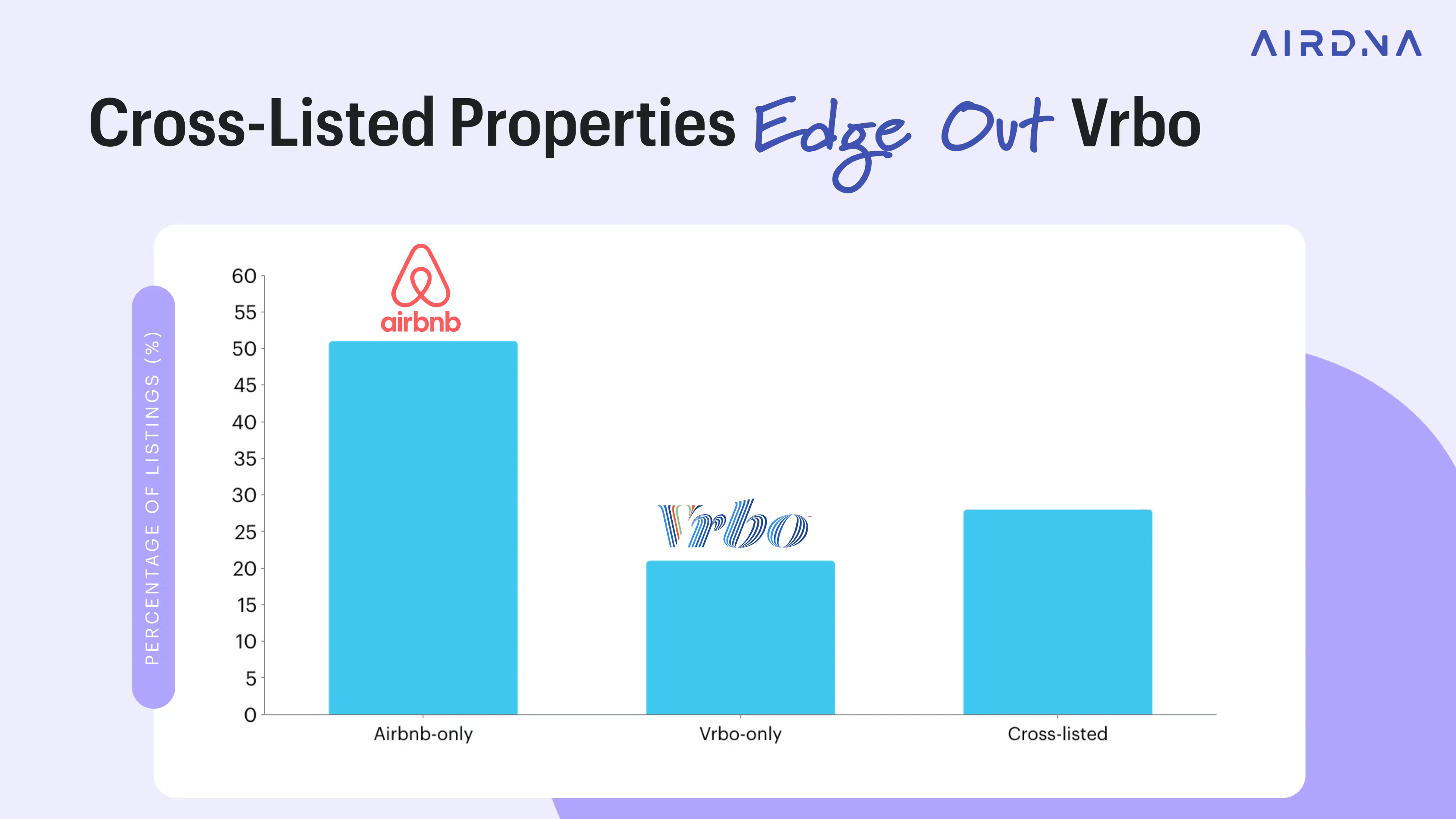

The vast majority of hosts still list only on Airbnb, though cross-listing has been rising. In the U.S., professional operators—defined by AirDNA as those managing 21 or more listings—cross-list at rates of roughly 60%, versus around 21% to 28% for non-professional hosts.

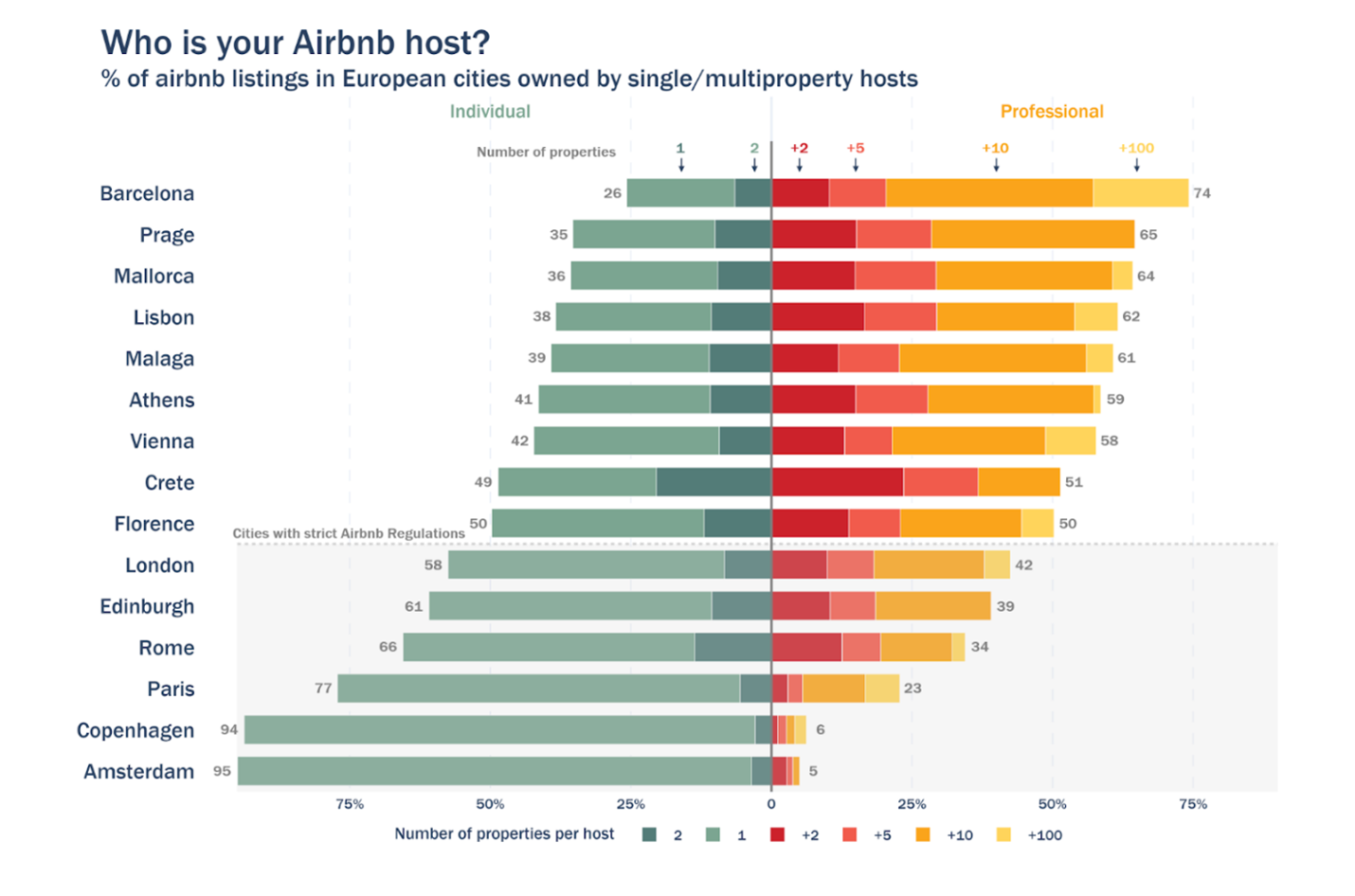

The mix between individual and professional hosts is shaped in large part by local regulation, a theme we will return to later. You can see this clearly in the chart below, which shows the supply mix across major European cities as of early 2024.

Competitive Landscape

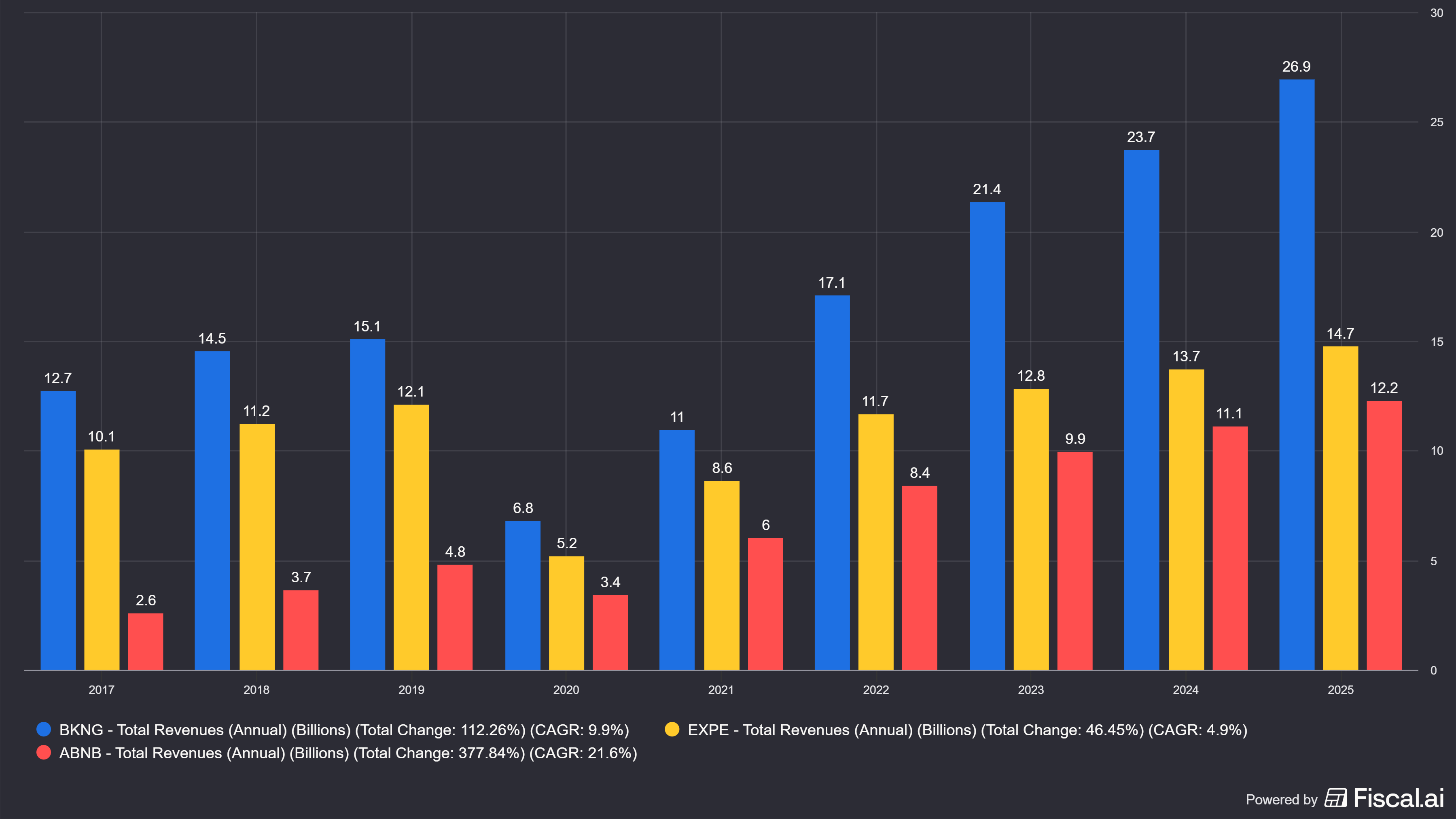

The short-term rental market is effectively an oligopoly. Airbnb, Booking.com, and Expedia—which owns Vrbo—controlled roughly 71% of the market in 2024, up from 53% in 2019.

Booking and Expedia are traditional online travel agencies (OTAs), offering hotels, vacation rentals, flights, car rentals, and other travel products. Their inventory is also more professionalized, spanning hotels and large property managers. Airbnb and Vrbo are more narrowly focused on short-term rentals, though Airbnb’s expansion into hotels, services, and experiences is beginning to blur that distinction.

Accommodations account for the bulk of revenue at both Booking and Expedia, at roughly 90% and 80%, respectively, with the remainder tied to flights, car rentals, and other products. Booking also has the highest effective take rate, averaging roughly 14.4% over the past two years, compared with about 13.5% for Airbnb and 12.3% for Expedia.

Booking is particularly strong in Europe, where it holds roughly 48% share, versus about 40% for Airbnb and just 2% for Vrbo. In the U.S., the pattern reverses: Airbnb leads with roughly 43% share, followed by Vrbo at about 21%, while Booking trails at just 8%.

Vrbo occupies a narrower but still defensible niche. Its supply base skews toward entire homes, and its customer base over-indexes toward families, group travel, longer stays, and older travelers. That positioning gives Vrbo a clearer identity than its relative scale might suggest.

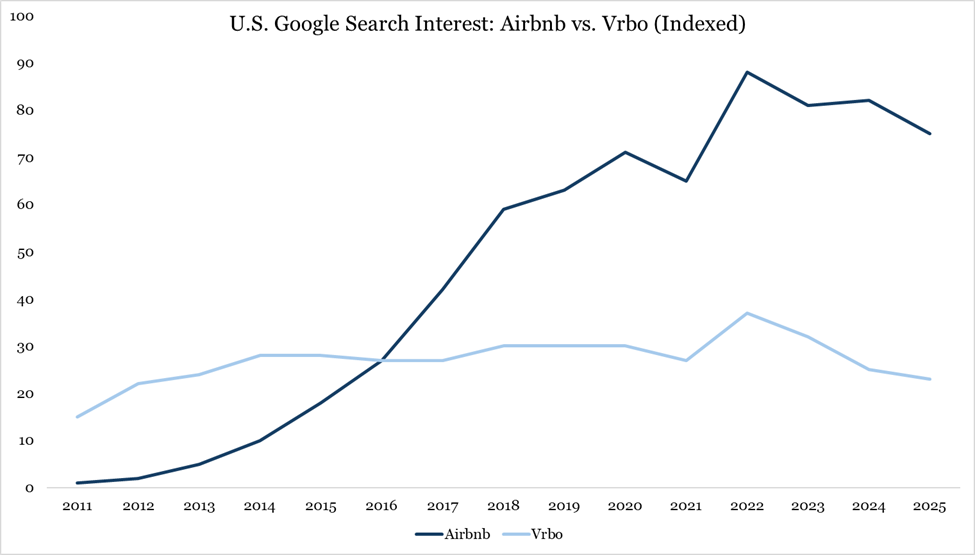

Still, the long-term trajectory is hard to miss. Despite a 13-year head start, Vrbo was overtaken by Airbnb within a few years. Today, Airbnb is roughly three times larger by revenue. Google Trends provides an imperfect but useful proxy for that shift.

Today, though, most bookings happen through apps—and Airbnb leads there as well. In 2025, roughly 64% of its bookings came through mobile, versus figures in the mid-50s for Booking and Expedia.

The Moat(s)

“Airbnb” has become nearly synonymous with short-term rentals. Guests rarely say they stayed in a vacation rental; they say they stayed in an Airbnb. Outside of Vrbo in the U.S.—and even there, to a much lesser extent—no competitor enjoys anything close to that linguistic hold.

Airbnb has even crossed the threshold from noun to verb: the pinnacle of brand strength. Naturally, it has leaned into this in its marketing: “Now you can Airbnb more than an Airbnb.” That brand strength shows up where it matters: since the pandemic, roughly 90% of Airbnb’s traffic has come through direct or unpaid channels—well ahead of peers.

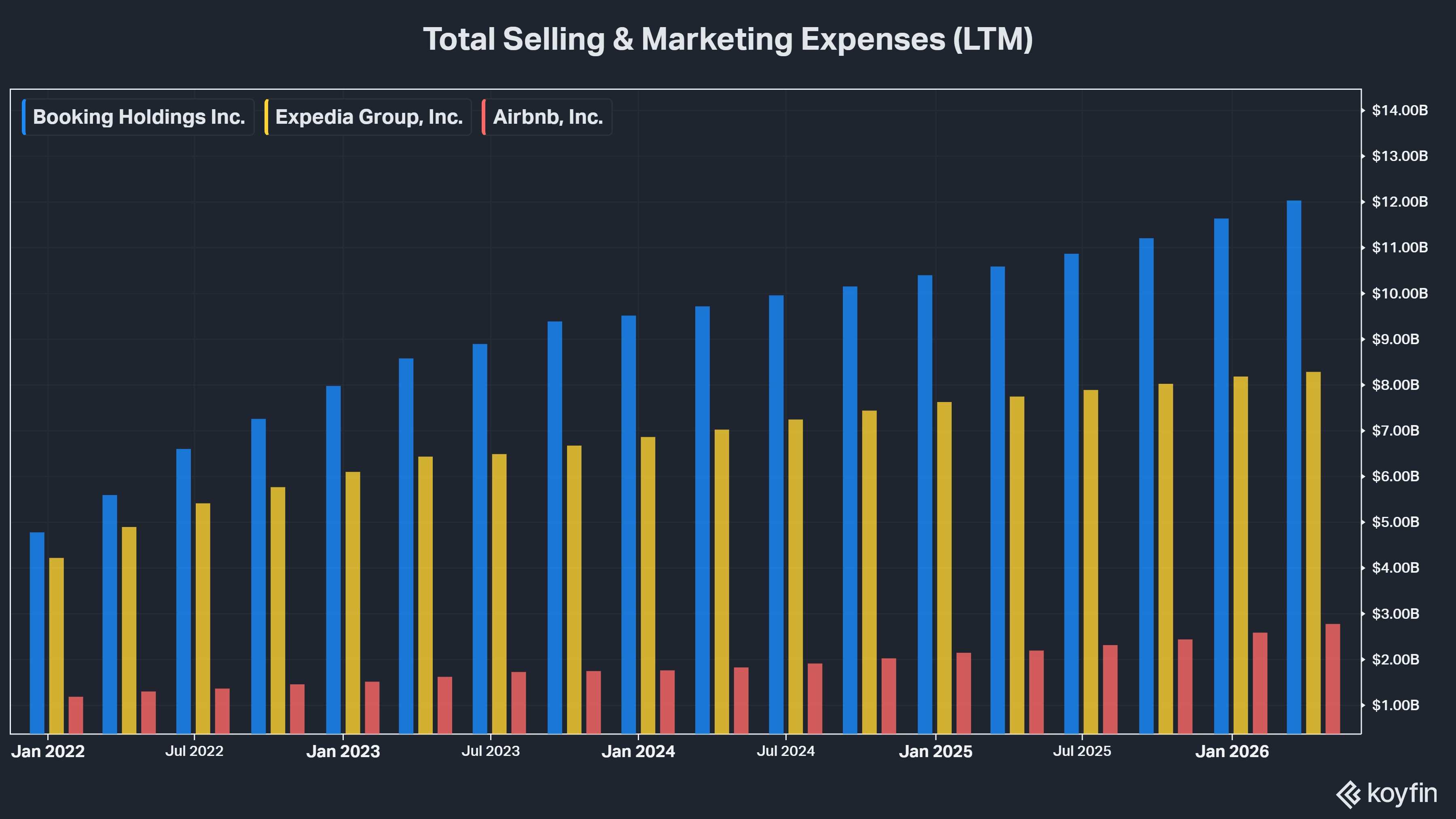

The P&L implications are not subtle. In 2025, Airbnb spent about $1.6 billion, or 13% of revenue, on brand and performance marketing. Booking and Expedia, by contrast, spent roughly $8.2 billion and $7.3 billion, respectively—or about 30% and 50% of revenue—using the most directly comparable measures. This is sometimes called the “Google Tax,” and Airbnb pays far less of it.

What makes this brand moat especially notable is how it was built—without the the bundles and convenience offered by traditional OTAs. No flights. No car rentals. No loyalty program. And, until recently, virtually no hotels. That said, each of those categories will likely prove necessary if Airbnb is to become the “one-stop shop for travel” Brian Chesky envisions—a point we’ll return to later.

Beneath this moat sits a classic marketplace flywheel. Greater supply—especially when it is unique and high-quality—drives more demand. More demand, in turn, makes the platform more indispensable to hosts, drawing in still more supply. That deeper supply base improves price competition and, critically, gives Airbnb more flexibility to shape the marketplace itself.

The company has leaned into that advantage aggressively. Since 2023, Airbnb has been “elevating the top and cutting the bottom,” as Chesky put it, removing more than 550,000 lower-quality listings while promoting “Guest Favorites,” its top 10% of listings by rating. Those listings now account for roughly half of bookings.

The result has been fewer support interactions and better booking conversion. Together with a broader set of product changes designed to reduce friction, these improvements have helped push Airbnb’s NPS to its highest level since the pandemic—“by far,” according to Chesky.

This selectivity advantage, combined with Airbnb’s disproportionate share of non-professional hosts, has lifted the average listing rating to roughly 4.8 out of 5 stars. Competitors do not disclose directly comparable figures, but the gap is visible. In my own cross-platform analysis across major tourist cities, weighted-average ratings for first-page OTA results tend to fall around 4.2 to 4.3—and slightly lower when hotels are included.

Summing it up: better supply → better experience → more demand → greater selectivity → even better supply. That, in a nutshell, is the Airbnb flywheel.

There are, however, two further advantages that help keep it spinning.

1. User Interface (UI)

Spend a few minutes on each of the major platforms and the difference is hard to miss: Airbnb’s product is, by some distance, the most pleasant to use. That has been true for years, and it is likely to remain true. There are several reasons.

First, two of Airbnb’s three co-founders, Chesky and Gebbia, came from design backgrounds. But this is more than a matter of education or training: they live and breathe design. It is part of their DNA and, by extension, the company’s. As Chesky put it:

“I obsess over our app: its design, its interface … Everything must be perfect.”

Second, Airbnb is, unlike its competitors, a technology company operating in travel—not the other way around. The distinction can sound cliché, but it explains a great deal. By all accounts, Airbnb has some of the strongest technical and design talent in the world, helped by its San Francisco base and reflected, not coincidentally, in its materially higher SBC.

Finally, design quality is simply something Airbnb has chosen to optimize for—even at the expense of near-term conversion. That stands in contrast to its OTA rivals, where conversion is the organizing principle.

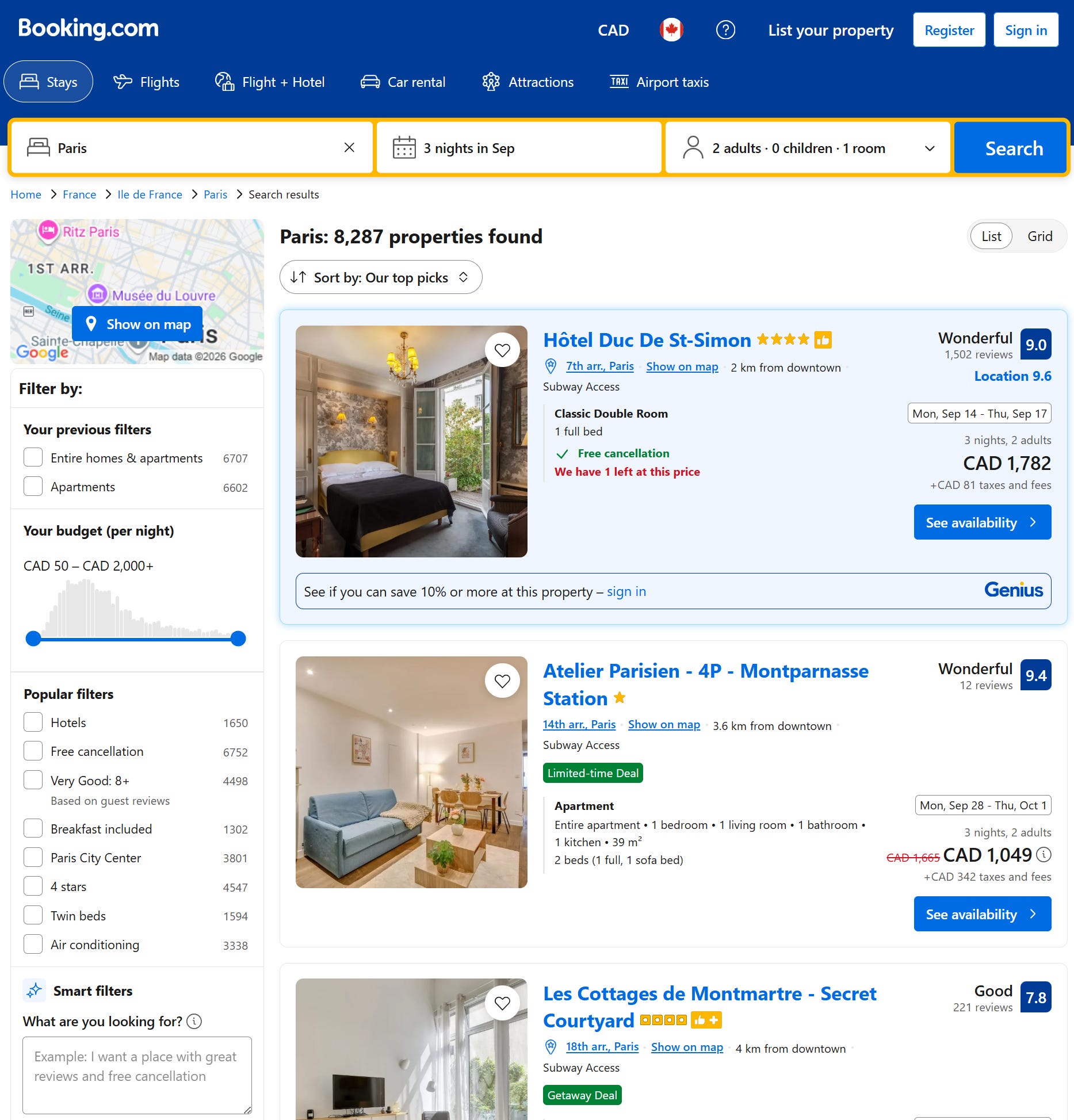

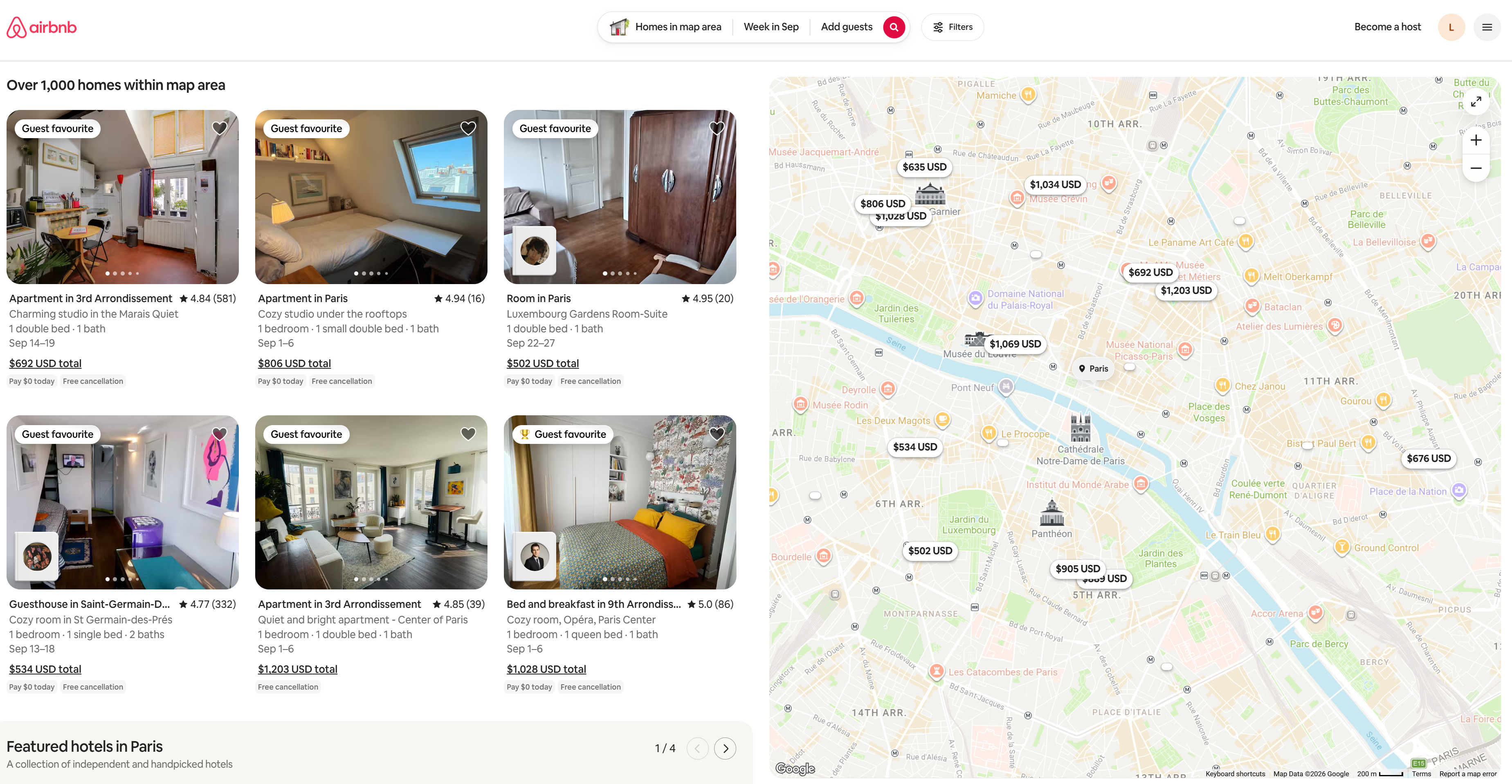

Below are comparisons of Booking’s and Airbnb’s webpages, both at 100% zoom, followed by a few brief observations.

It is not a knock on Booking to say that it feels, by comparison, like a high-performance marketplace funnel—because that is exactly what it is. The classic e-commerce persuasion cues are all there: urgency prompts, competing colors and font sizes, icons, badges, and so on. Meanwhile, the prominently featured filters nudge the user to narrow the search if the “top picks” do not appeal.

Airbnb does the opposite. The filter button is discreetly tucked away. The wider layout gives the page more breathing room. There are fewer visual interruptions, stronger aesthetic cohesion, and a general sense of openness. The experience feels less like shopping and more like browsing. The page seems to have one job: make the listings look appealing.

The contrast is just as clear at the listing level.

This “beautiful merchandising,” as Chesky describes it, directly reinforces Airbnb’s core advantage: having the largest catalogue of unique (i.e. non-commoditized) supply.

The second advantage is less tangible, but no less important.

2. Community and Trust

Reviews are a form of currency—proprietary reviews, that is—and Airbnb has more than 500 million of them. Engagement is unusually high, with roughly two-thirds of guests leaving a review after a stay, and those reviews tend to be longer and more detailed.

That is not accidental. It is a direct consequence of Airbnb’s deliberate effort to foster a sense of “community”—a word that can sound soft until one considers what the product actually requires: persuading people to stay in, or hand over, private homes.

Unlike other platforms—where, as Chesky has noted, “you often don’t even know who people are”—Airbnb profiles are rich and consistent. Users have profile photos, visible review histories, trip counts, and tenure on the platform. None of these are shown in quite the same way on Vrbo or Expedia.

Booking does somewhat better, displaying country of residence and profile photos. But unlike Airbnb, where profile photos generally show the actual user, adoption remains limited.

At first, these differences may sound minor. Then you see them.

Compared to Booking, top, and Vrbo, bottom:

These small touches combine to produce a not-so-small effect: Airbnb feels warmer, more personal, and less transactional.

More recently, the company has even started allowing users to see who else has signed up for a group Experience—and even to message those users afterward. As a result, Airbnb is beginning to look less like a traditional travel marketplace and more like a social platform layered onto one.

That helps reduce uncertainty on both sides of the transaction—something especially important when one of the top concerns for would-be hosts is the idea of a stranger staying in their home.

On Airbnb, guests feel less like strangers.

Closing Note

And that’s a wrap for Part I. Hopefully, readers now have a better understanding of how Airbnb’s marketplace works—and why its competitive position is stronger than the market often appreciates.

Part II, however, is where things get more interesting. There, we’ll examine the reacceleration case in both the core business and new verticals, address the key bear arguments—my favorite part—and walk through valuation, catalysts, and related considerations.

The valuation discussion is especially relevant now, given Airbnb’s rally and Booking’s sell-off. As many readers will know, Booking has become an increasingly obvious candidate for value-oriented investors, given its stronger recent growth—off a larger base—and materially higher profitability.

Thanks for reading, and stay tuned.

Glad to come across another investor long on Airbnb. I went long in August 2024 and have only gained conviction over time as they launched the new businesses and the stock didn’t react.

In terms of competitive advantage, I think the new ventures also position the firm as a platform where the incremental cost of new business lines is effectively zero, creating a very high flow through.

The company also has a great value proposition for hosts, given their service has a lower take rate for property managers while offering more property management services and insurance. It really is a no brainer for hotel operators to choose ABNB over Booking or Expedia.